The Home Loan Process

Demystifying Home Loans

Understanding the Home Loan Process: Expert Guidance from Pre-Approval to Closing

If you’re new to buying a home, the home loan process can feel overwhelming. I am here to keep you informed every step of the way — from pre-approval to closing day.

The first crucial step is to consult with a trusted mortgage specialist who can evaluate your financial situation and guide you toward the best loan options. If you don’t have a lender yet, I work closely with some of the top mortgage lenders in the industry and can connect you with a reliable expert who will prioritize your needs.

With the right team supporting you, navigating your home loan becomes smoother and less stressful.

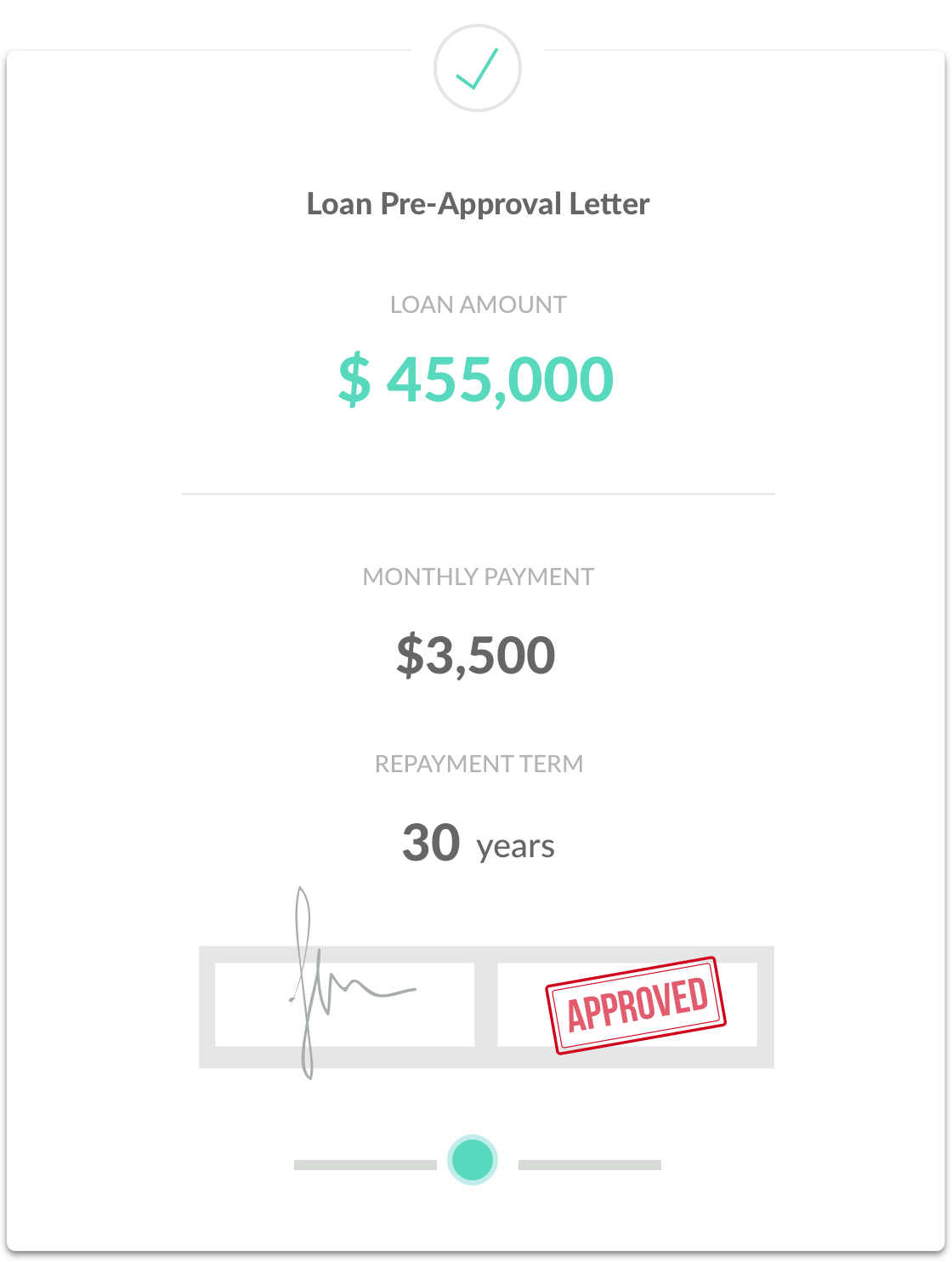

Get Pre-Approval

Why Getting Pre-Approved Is the First Step in Buying a Home

Before you start searching for your dream home, it’s smart to get pre-approved for a mortgage. Meeting with a Loan Officer early helps you understand exactly how much home you can afford — and shows sellers that you’re a serious buyer.

During the pre-approval process, your lender will review your financial information, including:

-

Income and employment history

-

Assets and current debts

-

Credit report and credit score

-

W-2 forms, pay stubs, tax returns, and bank statements

This helps determine your loan amount and which mortgage programs fit your needs — from conventional loans to FHA, VA, or first-time homebuyer programs.

Getting pre-approved not only saves time when house hunting, it also gives you a competitive edge when making an offer.

ESTIMATE YOUR MONTHLY PAYMENT

Estimate your mortgage payment, including the principal and interest, taxes, insurance, HOA, and Private Mortgage Insurance.

Price

Annual Tax

Loan Term (Years)

Down Payment %

Interest Rate %

Monthly HOA

Monthly Insurance

$3,198.20

Estimated Monthly Payment

Principal

$2,398.20

(75.0%)Taxes

$500.00

(15.6%)HOA

$100.00

(3.1%)Insurance

$200.00

(6.3%)Get Today's Daily Mortgage Rate

Learn moreWe Help You Get The Best Loan

Start The Process

We’ll help you find the best local loan officer to get you competitive rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with a lender today!

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an underwriter, who reviews and approves the entire loan if it meets compliance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your loan is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the loan is recorded and you get the keys. Congratulations, happy homeowner!